Published: September 23, 2024

In Regan Capital’s view, the often-overlooked residential mortgage-backed securities (“RMBS”) market offers a far better risk/reward trade-off than any other sector of the fixed-income markets. This perspective is supported by many of the world’s top fixed income managers. While it may not always be apparent to investors, many of the largest active fixed income mutual funds are dramatically overweight mortgages. We looked at 40 of the largest active fixed income mutual funds by AUM, that together make up over $1.6tn in assets and found that the average allocation to MBS amongst these funds is over 46%. That’s almost 20% higher than their next largest allocation (corporates, 27%).

RMBS is one of the only asset classes that becomes safer as it approaches maturity as mortgages amortize over time. As borrowers make their monthly mortgage payment, the loans backing RMBS de-risk via principal paydown and home equity growth. Principal and interest cash flows are returned to RMBS investors, allowing their holdings to de-leverage and giving them the opportunity to reinvest the proceeds. The return of cash flows can continually be redeployed, enabling superior compounding and income generation. In contrast, traditional fixed-income vehicles, such as sovereign, corporate and municipal debt, become riskier as the obligations come due as issuers often must pay off the debt in full at maturity rather than over time (also known as balloon risk or refinance risk). The unique structure of RMBS provide flexibility in managing interest rate, credit and reinvestment risk within fixed-income portfolios. There are instances, based on the shape of the yield curve, where it would be beneficial to own bullet bonds versus amortizing bonds. However, this benefit must be weighed against the additional credit risk that comes with bullet bonds.

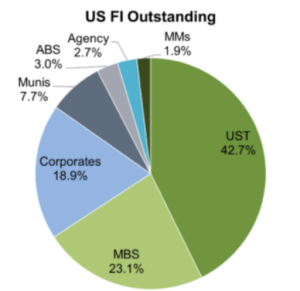

With total MBS issuance up significantly through 2024, the US residential real estate market remains one of the largest and fastest-growing markets in the world. $12.2 trillion of the existing mortgage market is held in RMBS, making it the second largest fixed income sector behind only US Treasuries.

With an estimated $1.9 trillion in new mortgages originations expected in 2020, the US residential real estate market is one of the largest markets in the world. $10.3 trillion of the existing mortgage market is held in RMBS, second only to the US Treasury market.

Approximately $8.8 trillion of the market is classified as Agency RMBS, while $1.5 trillion falls under non-agency RMBS. This primer will serve to lay out the enormous opportunity that exists in the US mortgage market and illustrate how an investor can concurrently add cashflow, reduce duration risk and ultimately add desirable diversification within a broader fixed income allocation.

Source: SIFMA.org

Another common strategy that investors use to manage duration risk is what is commonly known as a “bond ladder”. This is where an investor looking for regular income buys fixed-rate bonds that mature in regular intervals to fund future expenses. This strategy allows investors to manage the cash flow profile of their investment portfolio to support their future liabilities or investment goals. With fixed-rate, floating-rate, bullet, amortizing, and callable bonds now widely available in the fixed-income market, investors have even greater flexibility to build portfolios tailored to their unique cash flow needs. This adds another important dimension to portfolio diversification.

The shape of the yield curve often reflects investors’ expectations for the future path of interest rates. For example, when the curve is inverted it is a sign that investors expect lower interest rates in the future. While amortizing bonds may benefit from an inverted yield curve they will not benefit as much from the expected drop in interest rates as they generally exhibit shorter duration. However, there is a tradeoff that investors face between how much lower of a yield they accept for the extra duration and the benefit they get from amortizing bonds in an inverted curve environment. When weighing these tradeoffs investors can find that the benefits of compounding returns can make up a significant portion of yield differential that investors accept for taking duration risk. This means that amortizing bonds offer highly certain advantages over non-amortizing bonds in terms of managing duration risk.

In 2024, the market provided a great case study for managing a bond portfolio in an inverted yield curve environment. Most fixed income investors were certain the Fed would lower rates and bid up longer duration bonds to the point where mathematically it was highly probable that even if the Fed did lower rates, longer-duration bonds would not provide higher returns than shorter-duration bonds. Not only did that occur, but after the Fed lowered rates, longer-duration bonds decreased in price as the Fed disappointed market expectations for how much their influence on the front end of the curve would impact longer tenor securities.

Credit Risk

Another advantage that amortizing bonds provide comes in the form of lower credit risk. When borrowers repay their indebtedness over time, credit risk decreases as the bonds deleverage. Not only do investors have less absolute credit risk exposure, but also the exposure they have is higher quality, all else being equal, as the borrower has increased their equity position.

Credit risk in fixed income comes from the borrower’s ability to repay their indebtedness and is closely tied to the economy. When the economy contracts, we see borrowers, both corporations and individuals, default on their debt which directly impacts fixed income investors who own those bonds. When the economy is strong, investors receive an equivalent interest rate for taking on less credit risk.

At present, corporate bond risk premium is historically low as the economy has been strong, equity valuations are high, and equity investors have been moving into the relative “safety” of corporate bonds, which are higher in the capital structure than equities.

There is credit risk in the MBS market as well which comes in the form of different Non-Agency MBS. These bonds are backed by different types of loans to homeowners and secured by the real estate. Credit risk for secured bonds is generally lower than for unsecured bonds as borrowers possess equity in their homes, which can be seized and sold upon borrower default.

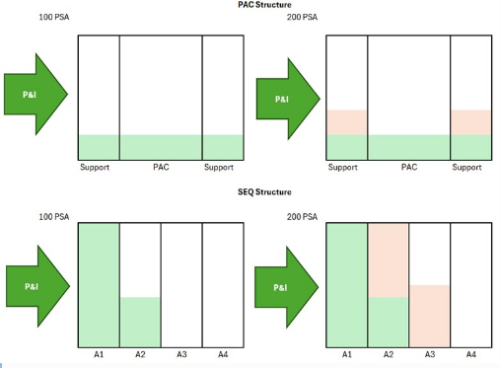

In this example, we see the two primary structures in the Agency MBS market: PAC and Sequential structures. PAC bonds are structured so that their cashflows and maturities are very stable, with the support bonds absorbing all the variability in cashflows. This allows PAC bond investors to buy a mortgage bond that is very similar to a corporate bond with a fixed maturity date.

The sequential structure allocates cashflows in sequence for different tranches which has the effect of making the first tranches in the sequence the shortest duration and the last tranches in the sequence the longest, since they have to wait for every tranche in front of it to be paid off before they get their principal back. All tranches receive regular interest payments at the same time.

Example: Time Tranching Cashflows by Repayment Priority

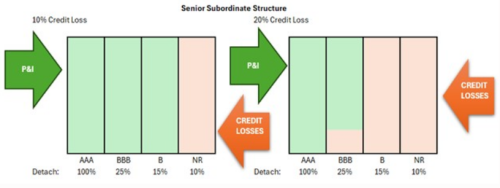

Similar to how Agency MBS are structured to provide different duration profiles, Non-Agency MBS are structured around the additional element of credit risk. The primary method for credit tranching is creating a senior-subordinated structure like the one pictured above. This is almost identical to the sequential structure in Agency MBS except that in this case the bonds are ordered in terms of priority of getting principal and losses. Principal is paid to the highest priority tranches first and are the last to take losses. Losses are taken by the lowest priority traches first and they are also the last to receive principal. This allows investment banks to take a pool of loans with an average credit rating of investment grade and create investment grade and non-investment grade bonds to sell to investors with different risk appetites.

Example: Credit Tranching